Physicians as 1099 employees have burst onto the scene as an enlarging workforce space and this has been spurred on by the growth of side jobs that are exploding.

Boom In Side Work for Doctors

1099 work is unfamiliar to many of you because you are increasingly being herded into W-2 physician employment.

Thus over the past decade, you and your peers have been progressively abandoning self-employment in favor of traditional employment.

In fact, if you want to look for a job right now, mostly all you would see on job boards are traditional employment options as W-2 workers, although some short-term locum opportunities such as 1099 work may pop up as well.

But there is now after the COVID pandemic, there is a boom in side jobs like telemedicine and virtual work and this has resulted in an uptick in non-employee 1099 income for many doctors. A recent Medscape survey indicates as much as 40% of doctors have side jobs on top of their primary job.

This why we have began to see the use of the term “1099 employee” more and more within the physician ranks. As I have noted in a previous blog post, there are numerous advantages to both physicians and large corporations to make you a 1099 employee—for both short-term and long-term work.

Non-employee compensation is paid by corporations to independent contractors who aren’t employees. From speaking with doctors all over the country it is increasingly common to see physicians having some combination of both W-2 and 1099 income. This is typically constructed as a primary job via traditional employment and a side job as an independent contractor.

Personally, I like receiving all of my professional earnings as a 1099 employee because of the tax advantages associated with my professional S-Corp. This includes my primary job via an employment lite agreement and also all of my side jobs such as hospital call and nursing home directorship.

The Old Normal Is Being Replaced

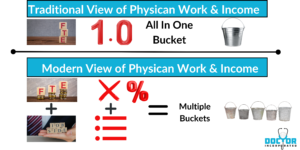

The old normal of one doctor, working one job, in one location is gradually being replaced by a mixture of active and passive income sources that all lead to a preferred lifestyle.

There was a time when a doctor’s life was dominated by their “call” to serve a localized population and many doctors lived within the glass house of “always being on”. Their personal life and professional life were tightly intertwined as many doctors sacrificed certain lifestyle considerations in exchange for fulfilling their professional ethos to serve. As a rural doctor, I have lived that life. There is no doubt that high income and community prestige lead to a good life—one that doctors have come to expect to live.

This romanticized view of a doctor’s life was a reality during the days when the practice of medicine was a cottage industry, but the times have dramatically changed as you no longer have control over the business of medicine. Thus most doctors will experience some sort of job change during their career and the likelihood of being at the same job for 10 years or longer is <20%.

For years this idea of working one job in one location was entrenched within the private practice model which then gave way to the traditional employment model. The latter offered a parallel promise of a stable and long-term location to practice medicine and live a good physician’s life—with the added twist of a very predictable high income without the stress and hassles of managing employees and small medical business that was no competing with large corporations.

Employment became the simplest way to transfer the mindset of one doctor with one job in one location. It has become the secure, predictable, and financially viable option for most of you—and it’s why 90% of new graduates are going this route.

There is the self-awareness that after years of nomadic training, you and your loved ones often look forward to finally settling into one location to begin living the doctor’s good life.—-no more delayed gratification, and no more moves. Throw in some financial incentives to erase your massive school loans and large employers can provide the perfect launch pad for beginning your career.

Disruptive Trends

But two broad trends converged to disrupt the mindset around employment in one location:

-

Disillusionment with Employment—The loss of professional autonomy, growing burnout rates, elevated taxes as W-2 workers, and the loss of control over your personal/professional life has forced many doctors to look for non-employment job options—including many who are abandoning the system altogether and doing direct care models with no 3rd parties

-

Gen Z and Millenials’ Evolving View of Work-Younger workers tend to work multiple jobs, work independently, and are skeptical about the security of employment. Gen Z tends to question whether they can find contentment in the traditional American lifestyle—that is employment focused. Gen Z tends to see themselves as entrepreneurs who wear multiple hats with flexible work schedules, working vacations, and more consideration for personal time. In the end, the preferred lifestyle is the mission/goal, and work and income are the means to get there. This is in contrast to baby boomers whose mission/goals were based on an intertwined job/personal identity that totally consumed them all which led to the downstream effect of a “good life”.

Impact On Young Doctors

These trends are influencing young doctors who are starting to question whether traditional employment is really best for them, and are starting their careers with a focal point of a preferred lifestyle and quality of life.

This informs and directs young doctors to a new, modern version of a medical career that is configured as one doctor working several jobs in several locations.

1099 income combined with W-2 income is the new normal

This is the new normal. The mixture of sources often is a combination of employment and self-employment jobs (W-2 and 1099 income). The combinations and practice locations & jobs change and evolve as the market and physician needs change and grow. In the modern model, long-term alignment with just a single employer is highly unusual and statistically unlikely.

Thus many modern doctors are receiving taxable income via a combination of income sources that can range from active (professionally generated) to passive (your money working for you) income channels.

Tax Considerations For W-2 and 1099 Income

Almost every doctor has the same concern about their income, and it goes something like this: “ I pay a lot in taxes—so I can keep as much of my earnings as possible and pay fewer taxes.”

Doctors will do all sorts of crazy things in pursuit of paying fewer taxes and keeping more of their earnings—this can range from cheating on your taxes (please don’t do this!) to moving to a more tax-friendly location. For instance, I know a doctor couple with a significant net worth and large passive income holdings who just moved to Puerto Rico as a strategy for reducing their tax burden. I am not advocating for this kind of thing-but tax arbitrage of different locations to live in does have some power depending on your specific circumstances.

So as you use your skills to hustle and add a few bucks to the pot, there are important tax considerations to know about with your non-employee 1099 income. I recommend you not wait until you do your taxes to explore this—cause by then it’s too late to deploy some of the tax strategies.

As I dive into taxes, let me start with the basics that will apply to every physician as an individual tax earner. These strategies are available to all regardless of what percentage of your income is W-2 or 1099.

High-Income W-2 Tax Lowering Strategies:

If are a traditional employee, like the majority of doctors, you can reduce your taxes with some of the following itemized deductions, assuming you don’t just choose standard deductions.

-

Tax Advantaged Retirement Accounts like 401(k), 403(b), and 457 plans just to name a few.

-

Child tax credit* *phased out for joint filing with >$400,000 in income

-

Child and Dependent Care credit* *% based on adjusted gross income

-

Mortgage Interest* *Mortgage interest deduction limit is $750,000 mortgage

-

Charitable Giving

-

Tax Loss Harvesting

-

State and Local Tax Deduction (SALT)

-

Medical Expense Deduction

-

Solar tax credit for residential clean energy

-

Electric vehicle tax credit

For high-income earners like yourself, many of these deductions are phased out or are reduced in value as your adjusted gross income rises.

The bottom line is that there are still some incentives in the American tax code to save money for retirement, be married, mortgage your home, have children, make charitable donations, as well as use clean energy. Due to these behavioral financial incentives created by our government, you should take advantage of them.

Your Best Tax Decision

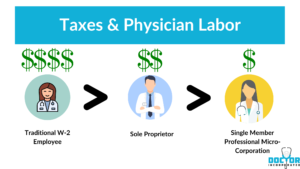

However, the best tax decision that a high-income W-2 employee can make is to start your own business because the non-employee income opens up so many additional tax strategies that are only available to small businesses. The most readily available, uncomplicated, and low-cost small business option for any doctor is to incorporate themself as a single-member professional micro-corporation.

So when I talk about starting a small business, let’s keep it simple and focused on what you have already earned and can easily start—without taking out loans, having a complex business plan, buying a retail storefront, etc…. Incorporating yourself is simple and has minimal overhead— but it unlocks all kinds of powers, including tax strategies.

To understand why a professional micro-corporation is a great tax strategy for a doctor, let’s take a brief look at employee and non-employee taxes.

Payroll Taxes For Employees and Non-Employees

Every U.S. taxpayer must pay Social Security and Medicare taxes on his or her income for both employee compensation and non-employee compensation.

For self-employed individuals, these taxes are called self-employment taxes. Self-employment taxes are calculated on the individual’s federal income tax return based on the net income from the business, including 1099 income.

From a tax standpoint, tax withholding is the primary difference between W-2 and 1099 employees:

-

Employees: Employers will take out various payroll taxes such as federal and state taxes from your paycheck for you, and they are obligated by the government to do this. Federal taxes are comprised of Social Security and Medicare taxes. Your withholding gives employees an automatic way to pay their taxes as they go. At tax time, you receive a form W-2 from your employer indicating how much you have earned and the amount of federal, state, and local taxes that have been paid.

-

Non-employee, or independent contractors: Your check won’t have any payroll taxes withheld. That means paying your taxes falls on YOUR to-do list. Most commonly this is done quarterly for both federal and state taxes. At tax time, you’ll receive Form(s) 1099-NEC to show the total amount you or your business were paid for the year, and the IRS will expect that you have paid the taxes on these earnings. Failure to do so will result in quarterly penalties, so don’t expect to just “square up” at the end of a tax year.

Independent contractors will pay taxes on the non-employee compensation quarterly via what is called estimated payments. That means four times a year, you’ll send an estimated tax payment to the IRS for federal taxes. You will also have to pay quarterly taxes to any applicable state and local revenue departments.

Depending on your skill set and time, you can do this yourself. But many will outsource it to a tax or accounting professional. That is what I do.

Self-employment and Schedule C

Your professional service related 1099 income will be considered self-employment income, and you will need to pay self-employment taxes. Social Security and Medicare comprise the federal taxes on your non-employee compensation. This is true even if you don’t file a Schedule C like most W-2 earners.

The schedule C IRS form is an important document for taxpayers who are self-employed or have a business. It is used to report income, expenses, and other related information relating to the operation of a business. This form is also used to calculate the net profit or loss from the business, which will be reported on your individual tax return. In addition, it can be used to claim deductions related to your business expenses and any losses incurred during the year.

You Do Want Access to Schedule C

But schedule C is what separates individual taxpayers as W-2 earners from the sole proprietor/single-member LLC owners and it’s important because allows you to deduct business expenses from your earned income. This allows you to significantly lower your adjusted gross income—and thus lower your taxes.

Traditionally employed doctors don’t get access to schedule C for their W-2 earnings, thus the options to lower your adjusted gross income are significantly less than if you received the earnings as 1099 rather than W-2.

Or, You Want Access to Deducting Business Expenses

Much like W-2 workers, single-member professional micro-corporations taxed as an S-Corp don’t have access to schedule C.

But that is ok because the actual business and S-Corp structure allow for business and benefit expense deductions through the small business’s tax structure/tax filings. The end result is that it lowers the owner’s overall tax burden.

S-corp owners ultimately have even more tax strategies available to them than sole proprietors due to the way the tax code is written. It tends to favor businesses over individuals.

Thus from the viewpoint of the tax drag on earnings, the following graphic summarizes things for you:

Based on this information, I highly favor forming a professional micro-corporation as an S-Corp and recommend that you receive all of your professional income in this way. By doing this, I have cut my effective tax rate in half, and retain $70,000-$100,000 in income annually—all adding up to a million dollars over 10 years.

Wouldn’t you like a million more dollars by simply working smarter, and not harder?

I recommend that you consult with a tax professional or business attorney to determine the best approach for your specific situation,

But here is a quick resource to rapidly check out how much money you could retain every year. Take a look at this free questionnaire at SimpliMD that will estimate your retained income potential in less than a minute.

I encourage you to find out how much money traditional employment is costing you every year and the amount you could save through wise business modeling through your own single-member professional micro-corporation.

[/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section]