Today I am picking up a continuation of my blog post from last week that began to unpack some of the tax advantages available to the 1099 employee.

I will warn you that this is a long post and we are gonna down the rabbit hole a bit. So hold on and follow closely as I summarize some complicated stuff and explain from a tax perspective why you should transition your income source (s) from traditional W-2 employment to as much self-employment and non-employment income as possible.

Take Home Message

Here is the take-home message of this post if you don’t want to read the whole thing:

-

I recommend you have multiple income channels in your life and the fewer that are W-2 employment-based, the better. Since the majority of doctors are now traditionally employed as W-2 employees, this has a wide application to over 500,000 doctors.

-

For those of you who have wisely understood the first concept and have already transitioned to 1099 employment, don’t get too smug because I am also going to help you understand why starting a professional micro-corporation for your 1099 income is far better from a tax perspective than the default mode of receiving your 1099 income as a sole proprietor.

-

Given the fact that many doctors now have a mixture of W-2 and 1099 income (side jobs), from a tax viewpoint, a professional micro-corporation is your best option for all or part of the active professional income that you earn.

A fundamental concept here is that you should have multiple income streams in your life. Just like diversifying your investment portfolio is important, so is the principle of diversifying your income streams. For a 5-minute overview of diversified income streams, check this out from the white coat investor.

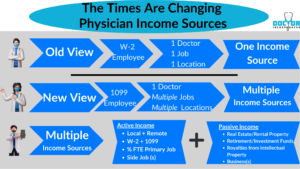

Changing Views of Physician Jobs

Doctors are prone to view their financial world solely through the lens of their active income earned through their primary job. This is reasonable given the size of the associated income, and given the intensity of the time demands associated with full-time medical work. It tends to be all-consuming and there is often little margin for anything else professionally.

However as I have previously stated in my blogpost “Physicians as 1099 employees”, the new world of physician labor is in the process of shifting from one doctor with one job in one location model to a more diverse model that includes multiple income sources from multiple geographic locations—that range from active to passive income— which all add up to meet a doctor’s preferred lifestyle and financial goals.

This graphic reviews the contrast between old and new views of physician work:

Multiple Income Streams

Personally, I have found that creating multiple income streams is extremely beneficial because it has provided flexibility, professional autonomy, financial security, and tax strategies throughout my career. It has taken me some time to create them and then stack them in the optimal business enterprise structure. But now all 9 of my small businesses function synergistically as my professional micro-corporation acts as a foundational component. Building the optimal business architecture for your streams of income is a critical concept and one that I will spend more time on a future post.

The idea of multiple income streams is one that is important for every doctor to understand, especially within the evolving world of physician labor.

To summarize there are 3 main types of income that most doctors will interface with:

-

Employment Income—this is your W-2 income that comes from being traditionally employed by a business. For doctors today this involves earning money from a large employer/hospital that pays you for your professional services. But technically W-2 income can also be generated by your professional small business.

-

1099 Self-Employment Income-this is 1099 contractor income that you earn through side jobs or via your primary job like with locums or employment lite. This is also called self-employment income.

-

Non-Employment Income- this is also known as passive income and most commonly is income earned through your sources that don’t require your physical presence. Simplistically this is how you use your saved dollars to make more money for you.

Though multiple active income streams may not be possible for many busy professionals, everyone can benefit from having a healthy mixture of both active and passive investment income streams.

In that context, let me share a brief summary of what I mean by non-employment income.

Non-Employment Income

Non-employment income is a great way to supplement your regular income, whether it’s from a full-time job or self-employment.

There are many different types of non-employment income available. Examples of non-employment income include rental property income, royalties from intellectual property, capital gains, dividends, & interest from investments, and profits from a business venture. Each type has its own advantages and disadvantages, so it’s important to understand how each can affect your financial success and tax strategies. Many call this “passive income” it is an important income stream for you to manage in your portfolio but it will not be the focus of this blog post.

I great example of passive income are the royalties that receive from my new #1 best-selling book called “Doctor Incorporated: Stop The Insanity of Traditional Employment and Preserve Your Professional Autonomy”.

As fun and diverse as it is, non-employment income will not be the focus of this post, instead, I am going to focus on your self-employment income as a 1099 contractor.

This income can either be earned through your primary job (employment lite) or through your side job(s). It is considered active income and requires your professional skills either physically or virtually.

Multiple Income Streams = Multiple Tax Channels

But where there is income earned, there are taxes. And this is where the new world doctor has to become a little more tax savvy as you stack multiple income sources. Because now you need to holistically look at the tax channels available to you for flowing that income through.

1099 Employee Taxes

So let’s drill down into the 1099 Employee space and talk about taxes. There is a lot to talk about here.

Self-employment Tax and Employment Taxes

Your professional service related 1099 income will be considered self-employment income, and you will need to pay self-employment taxes. Social Security and Medicare comprise the federal taxes on your non-employee compensation. This is true even if you don’t file a Schedule C.

The Schedule C IRS form is an important document for taxpayers who are self-employed or have a business. It is used to report income, expenses, and other related information relating to the operation of a business. This form is also used to calculate the net profit or loss from the business, which will be reported on your individual tax return. In addition, it can be used to claim deductions related to your business expenses and any losses incurred during the year.

Social Security Taxes Have A Cap

Social Security taxable wages are capped so that there is a maximum payment for each tax year. First, wages from employment are considered, then self-employment income, until the annual maximum taxable income level is reached. The taxable maximum for earnings in 2023 is $160,200.

No Ceiling on Medicare Taxes

There is no maximum on Medicare taxes, so all employment and self-employment income is subject to a Medicare tax of 2.9 percent but it is 3.8% for high-income individuals like you.

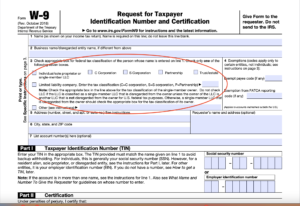

The W-9: Reporting 1099 Income

When you receive income for your work as a non-W-2 employee you must complete form W-9 indicating who will be responsible for the taxes.

The W-9 IRS form is an important document for both employers and employees. It is used to provide the Internal Revenue Service (IRS) with the necessary information to determine the tax liability of an individual or business. The W-9 form is also used to report payments made to a non-employee, such as independent contractors, freelancers, and consultants. By filling out this form, employers can ensure that their taxes are properly calculated and paid for on time. Furthermore, it helps employees track their income for tax filing purposes.

Are You An Individual or a Business?

The W-9 form assume gives you the option to be taxed as an individual or as a business. Due to the unfavorable nature of individual taxes for high-income earners, most of you will choose to be a business that is receiving the income for your work. The size of the business can range from a single-member business to anything larger. The size doesn’t matter to the government but the type of business entity does matter, because each of the business entity categories on Form W-9 has its own tax code rules associated with it.

Lines 1-2 on W-9

Line 1 needs completed regardless of your business entity

Line 2 needs to be completed if you have a business, but does not need to be completed if you are going to choose to receive the income as an individual or sole proprietor. Frankly, this can be a little confusing because sole proprietors get to act like a business through Schedule C, and furthermore, a sole proprietor can be incorporated or unincorporated. But most sole proprietors will leave this blank—make sure to check with your tax professional about this if you are a sole proprietor.

What you place in this line will be influenced by the remainder of this blog post, and your decision to choose a taxable entity for your income will come after you have thoroughly reflected on things in the context of your personal circumstances. None of this is “cookie-cutter”.

Just to be clear, due to your high income, it’s ok to check the box for in line 3 to be taxed as an “individual/sole proprietor/single member LLC but I recommend you never pay the taxes on this 1099 income as an individual/non-sole proprietor. That is because this income will be added to any W-2 income that you earn, and due to the progressive and tiered individual tax code—it will be taxed at the highest tax bracket that it is dumped into.

This is a common big mistake that doctors make, and it’s one that I hope to help you avoid.

Line 3 of W-9 Form

When you get to line 3 you have to make a single choice about the federal tax classification (and rules-tax code) that you want to be applied to these 1099 earnings. Each box has a separate tax code associated with it, which is why you have to choose.

Most individual doctors are going to default to receiving it as an individual/sole proprietor/single member LLC—which is ok—but honestly, most do it cause they are either unprepared to receive it any other way (ie: they have not started their professional micro-corporation), or they are just unaware of the other options. This box is kinda “safe mode” for you.

However, there are some compelling reasons to consider forming a single-member Professional Corporation (PC) or PLLC to receive this income through—-due to the additional tax strategies available to these tax entities that are not available to the sole proprietors. I will explain more about these differences later in this blog.

So again, hold that thought for now.

The First Check Box: Sole Proprietors and Single Member LLCs

If you are a sole proprietor or single-member LLC owner, you report 1099 income on Schedule C of your individual tax return—it is used to report “Profit or Loss From Business”. When you complete Schedule C, you report all business income and expenses.

Schedule C is an important form for sole proprietors to file their taxes due to the business deductions it makes available to you, which is not available to the individual taxpayer.

It is used to report the income and expenses of a business run by one person. This form helps sole proprietors to calculate their net profit or loss from their business that is solely based upon them individually. It is then connected to and reported for tax purposes to your individual tax return. You get to skip filing a separate tax return for your business—kinda nice. The information reported on Schedule C will also be used to calculate any self-employment taxes that may be due.

The net income from your Schedule C is reported on Line 3 of Schedule 1 of your personal income tax return along with all other sources of income, including income as an employee and investment income. Your personal income taxes are then determined by your total adjusted gross income.

Total Adjusted Gross Income & The Changing Views of Physician Jobs

Given the new view of physician work previously mentioned in this blog, this convergence of different taxable incomes on your individual tax return is going to become increasingly common.

Although your overall goal may be to “make more money” through your multiple income sources, you and your tax professional must always keep your eye on the “total adjusted gross income” line on your individual tax return. Failing to monitor this is common for hard-charging doctors who love to be high performers. The more the better, right?

Wrong, because your high income places you at risk for snowballing your taxes and the reality is “more money means more taxes”, especially if you simply receive it as an individual (don’t do this).

Before I became fully aware of all this, and I foolishly received ALL of my income through W-2 employment, I now understand why my accountant always looked at me incredulously when we sat down to do my individual taxes and while parsing my W-2 form he would sigh and say “Doc why did you make MORE money this year?”

Of course, being a driven high performer, I would smugly think to myself “What’s the big deal, I triumphantly made MORE money”, surely that is always a good thing. I was wrong.

That’s because I was tax naive, and didn’t fully understand the value and importance of the “total adjusted gross income” box as my seasoned accountant did.

Perhaps you too fall into the trap of thinking more earnings are always better.

I don’t want you to make the same mistake I made.

Therefore, sit down with your tax professional and discuss every legally compliant strategy that you can use to lower your “total adjusted gross income” including the best way to receive your 1099 earnings. The end result will be an ability to retain more of your hard-earned income.

The Other W-9 Check Boxes: Corporations

If your business is a partnership, multiple-member LLC, or a professional corporation, your 1099 income is reported as part of your business income tax return rather than on your individual tax return.

That is what I do through my professional micro-corporation in my employment lite agreement. Basically, all of my professional income flows into my corporation including my primary job and side jobs. This gives me much greater control over the flow of dollars that land in my individual tax return, which is a fundamental small business tax saving component. The tax savings in this professional small business model are scalable and grow larger as your 1099 income in the business grows larger.

Tax Payer Identification Number: Part 1 of W-9

After you complete lines 1-7 on the form, you will encounter what is called the Tax Payer Identification Number (TIN) which ultimately tells the government who will be responsible for reporting the 1099 income as well as who will be the responsible party to pay the taxes.

If you use your social security number, the IRS will assume you are an individual/sole proprietor/or single member LLC. This means the reporting and taxes will be connected to your individual tax return.

All other business entities will use an employer identification number and the reporting and taxes will be connected to the business’s tax return.

Your Choices For Taxation For Non-Employee Compensation

The fundamental question that every one of you who earns 1099 compensation for your professional services must decide is whether you should file your 1099 non-employee compensation as a sole proprietor/single member LLC or as a business/corporation, such as a single member PLLC or PC.

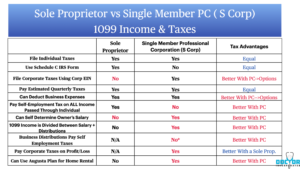

I advocate for every doctor to form a single-member PC or PLLC elected as an S-Corp, so let’s compare this to a sole proprietor/single-member LLC.

The answer to the question about which is better for you depends on your specific circumstances, including your taxes. Here is a breakdown of a compare and contrast for small business owners trying to make their decision.

As you can see from the comparison, doctors are typically better off forming a single-member PLLC or PC and electing to be taxed as an S Corp.

Since we are focusing on taxes, let’s do deep dive comparing the two options. The following graphic delineates some factors for you to consider between a sole proprietor and a professional micro-corporation taxed as an S Corp. I will explain and unpack this further as we go.

Individual Taxes & Adjusted Gross Income

As you can see in the graphic, both sole proprietors and single-member professional corporations taxed as an S-Corp will have to pay self-employment taxes. The options to lower your “adjusted gross income” are basically the same as those available for all W-2 employees.

The Sole Proprietor

But the sole proprietor does have a special tax lower tool in their arsenal and that is Schedule C because it allows them to lower their adjusted gross income via business expenses.

But the key difference is that sole proprietor has no way to lower the $$ amount that gets placed in the top box of their income reporting on their individual tax return. So although Schedule C is in play, the starting dollar value is high. These starting dollars are what will be subject to self-employment taxes.

The Single Member Professional Micro-Corporation

In contrast, your single-member professional micro-corporation owner has the built-in business structure to lower your taxable income in the top box of your individual taxes, and this structure can lower it by as much as 40%.

The result of having your professional micro-corporation receive the income FIRST is that you now gain access to the following tax strategies:

-

Control over the $$ amount of your income that will be taxed. Thus you have the power to lower the $$ that ends up in your household as earned income. (don’t worry—as I will explain later-businesses have multiple channels for getting $$ tax efficiently into your household)

-

Greater tax lower strategies than the sole proprietor/Schedule C option that further reduce your “adjusted gross income”. That is because the tax code favors businesses over individuals—it’s just a hard cold fact

The end result with a professional micro-corporation is that you will have greater power to lower your “adjusted gross income” and thus end up with significant tax savings compared to the sole proprietor.

Let me explain how this works even further.

Self-employment Taxes

-

As a sole proprietor, you are responsible for paying self-employment taxes on ALL of your income. This tax is currently set at 15.3% and is made up of both the Social Security and Medicare taxes, with a cap on the social security component.

-

In contrast, professional micro-corporations as S-Corp owners can receive both a salary and distributions from the business and only the business owner’s salary is subject to self-employment tax. Corporate distributions (profits) are not subject to payroll taxes.

Thus your earnings are routed to the business first and then it is broken down into two channels and the recommended ratio from most accountants is to keep salary at 60% of the earnings and distributions at 40% of the earnings. With your large income, this creates quite a bit of tax savings through the combination of the two.

-

Salary—your self-employment salary is subject to payroll taxes, but by lowering your salary through your own corporation you will pay fewer taxes in comparison to receiving it all as a self-employment salary (like a sole proprietor).

-

Most professional micro-corporation owners will set their IRS-compliant “reasonable salary” at a rate lower than their 1099 earnings and thus lower their tax rate on their earned income compared to receiving it as a sole proprietor or as W-2 income.

-

-

Distributions-these are not subject to payroll taxes but will be taxed as pass-through income on your personal tax return through what the IRS calls a K-1 schedule form.

-

In summary, when you file taxes as a corporation and take the S-Corp election, you can split your income between salary and distributions. Both are taxed at ordinary income tax rates, but both are NOT subject to employment taxes. Only salary is. Imagine someone who earns $400,000 and files as an S Corp with a salary of $200,000. They can save $200,000 worth of 3.8% Medicare fees = $7,600 per year in taxes, without decreasing any Social Security or Medicare benefits. Thus In this situation, you are reducing the overall tax drag of those earned dollars in comparison to the sole proprietor (and traditional W-2 employed doctor)due to the way they flow to you as S Corp distributions rather than salary.

-

-

For professional micro-corporation S-corp owners, unlike sole proprietors, it is the combination of salary and distributions that will create the most tax-advantaged blend to land dollars from your earnings into your household bank account.

-

Growing your household bank account is the end goal (net worth) for all of us, and the professional micro-corporation provides the optimal way to do this for a high-income earner. The secret sauce is in the flow of dollars through multiple channels in comparison to the single channel of the W-2 worker or the sole proprietor.

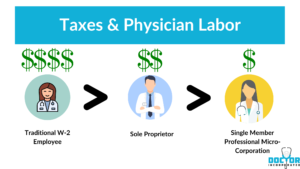

Stated bluntly, you are a sitting duck for the IRS if you are a traditionally employed W-2 physician. The government loves you, especially if you make over $400,000. As a high-income earning professional, you should try to avoid receiving your earnings as a W-2 worker.

Let’s take a closer look at each of these job structures and how they affect your income taxes.

Income Taxes

-

W-2 employees will pay taxes on all their professional earnings with little ability to reduce the tax burden by lowering their “adjusted gross income”. This is the worse spot to be in, and every tax return you complete is a reminder of this. Take home message is that although the financial and other incentives to be a traditional employee are strong, the back end of this decision, especially in regard to taxes comes at a high cost. There are better options out there than traditional employment!

-

Sole proprietors receiving non-employee income will pay taxes on all their professional earnings but will have the added benefit of being able to deduct more business expenses through Schedule C, which lowers their adjustable gross income in comparison to W-2 earners. They also maintain the same tax-lowering options as W-2 workers that I mentioned to start this blog since they report their business income and expenses on their personal tax returns. All this leads to significantly more tax savings in comparison to the traditionally employed W-2 doctor and allows them to retain more of their hard-earned income.

-

Professional micro-corporation S-Corp owners file a separate tax return for the business, in addition to the owner having a personal tax return.

-

Since the business owner still does an individual return, he/she has the same tax-advantaged personal deduction options as the W-2 worker and sole proprietor do on their personal tax return.

-

But the S-Corp business owner can take things a step further than the sole proprietor to reduce their gross income through the combination of salary and distributions previously mentioned. Professional and business expenses are still deductible but are contained in the business’s profit/loss/distributions. Within this space, S-Corps have more tax-advantaged strategies than those afforded sole proprietors in their individual tax forms.

-

S-Corps can pass through business income and losses to their owners, who report this on their personal tax returns via the K-1 form. This means that the business’s profits are only taxed once, at the owner’s personal tax rate. The goal for most professional micro-corporations is to have the business earn very little profit annually (pay less corporate taxes) all while the corporation shoulders your professional expenses and fringe benefit programs, pays your salary, and provides you with owner distributions.

-

The decision of what to do with your corporation’s profits can be a bit of a tax puzzle at the end of any tax year and can range from:

-

re-investing it in the business

-

paying a bonus salary(federal mandated 22% tax)

-

receiving it as a profit-sharing contribution into a 401(k) which is not taxed, does have federal limits, and is a deductible business expense

-

Taking a distribution that will be taxed as pass-through ordinary income to the owner.

-

The answer to which is best depends on your individual tax structure each year. As my accountant always says: “It’s a game-time decision every December”.

-

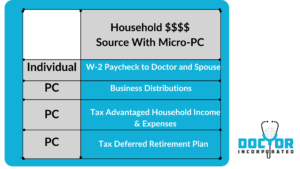

-

It’s the combination of these business-related money channels that all bring dollars into micro-business owners’ households in a more tax-friendly manner than if you simply were paid the same dollars as a W-2 employee or sole proprietor. This is what those 4 basic channels of cash flow look like in the professional micro- corporation’s home.

-

The tax-advantaged household income and expenses that flow through your single-member professional corporation ultimately create a blend that can benefit your household via tax-free income channels all while reducing your business’s taxable corporate profits. A good example of this is the Augusta Rule which you cannot take advantage of if you’re a sole proprietor. You need to have an LLC or Corporation that is taxed as an S-corp, C-corp, or Partnership and set up with a separate EIN.

-

Putting It All Together

In general, if you are just starting out and have limited liability exposure, filing as a sole proprietor may be simpler and more appropriate. However, if your personal assets or business has significant liability exposure, then forming a separate micro-business entity may be more appropriate. While not a direct tax advantage, it’s worth noting that professional micro-corporations as S-Corps offer limited liability protection to their owners, which means that the personal assets of the owners are generally protected from business liabilities and debts. For high-net-worth individuals like doctors, this is a significant advantage over sole proprietors.

Professional micro-corporation as S-Corp owners can take advantage of certain tax deductions that are not available to sole proprietors, such as health insurance premiums and certain retirement plan contributions. You can save taxes by hiring your family members, you can use special tax deductions like paying for your child’s private education and leasing a car. Ultimately all of these business advantages and fringe benefits are what my wife and I have done with my blog business, our real estate business, and my professional micro-corporation. The tax advantages have been massive.

Back To The W-9 Form

So in preparation for completing a W-9 form someday, and now knowing what you know about all the options available to you for your 1099 income, most doctors will need to first decide if you want to receive it as a sole proprietor or as a professional micro-corporation. Both have their advantages and disadvantages.

Please don’t make the common mistake of simply receiving the 1099 income as an individual only. This rookie move will cost you a lot of money in taxes.

I highly favor forming a professional micro-corporation as an S-Corp and receiving all of your professional income in this way.

This will require you to start your own professional micro-corporation ahead of time, which will include an employer identification number (EIN). All of this will be needed for your W-9 form lines 1-7 and Part 1.

I recommend you do this BEFORE you come to this fork in the road. Meaning do it now, even if you don’t yet receive any 1099 income—cause given the changing physician labor market, you will eventually earn 1099 income in some way.

I recommend SimpliMD for helping you start a professional micro-corporation as they specialize in helping doctors do this all over the country.

Your Decision Could Save You Millions of Dollars

By doing this, I have cut my effective tax rate in half and retained $70,000-$100,000 in income annually—all adding up to a million dollars over 10 years.

Wouldn’t you like a million more dollars by simply working smarter, and not harder?

I recommend that you consult with a tax professional or business attorney to determine the best approach for your specific situation.

If you want to check out how much money you could retain by switching your earnings from traditional employee W-2 to 1099 employee income check out the free questionnaire at SimpliMD that will estimate your retained income potential in just a few minutes of your time. Check it out and discover how much you can save through wise business modeling.