[et_pb_section fb_built=”1″ theme_builder_area=”post_content” _builder_version=”4.20.4″ _module_preset=”default”][et_pb_row _builder_version=”4.20.4″ _module_preset=”default” theme_builder_area=”post_content”][et_pb_column _builder_version=”4.20.4″ _module_preset=”default” type=”4_4″ theme_builder_area=”post_content”][et_pb_text _builder_version=”4.20.4″ _module_preset=”default” theme_builder_area=”post_content”]

40% of Doctors Have Side Income

We all know the growing majority of doctors are traditionally employed, and a recent survey has revealed that a staggering 40% of doctors have side jobs, despite the fact that they already have full-time jobs. This is due to the fact that taxes are taking a heavy toll on our income, leaving us with no choice but to look for additional sources of revenue. As a result, many of you are now relying on side hustles and other means of generating extra income in order to make ends meet.

There are two main types of side jobs:

-

Through your primary employer

-

Outside of your primary employer

Wanting More Income

For the traditional employee, the subject of compensation commonly comes up with your first or second contract extension, the timing of which often correlates with your enlarging household spending that is associated with the early part of your career. Children alone amp this up with the current cost per child to a middle-income married couple being an extra $14,800 per year and an eighteen-year total of $267,000.72.

Whether it is due to children, cars, a home, vacations, or loans, you will likely find yourself looking for ways to grow the flow of dollars into your home.

Your first response will typically be to figure out how you can increase your income through your primary job. You will note that your employer has made provision for this through either a productivity bonus structure or through basic productivity-based compensation models that incentivize you to earn more income by producing more wRVUs. It’s a pretty simple formula: do more work for your employer and they will pay you more.

Starting With Your Employer

If you approach your employer about compensation, they will remind you that they are constrained by federal laws to keep your payment within a fair market range, and thus can’t negotiate an increase in your productivity-based compensation. This is the fundamental reason they have a productivity-based compensation matrix for their employees—it is standardized and federally compliant. Additionally, it would be unfair to your fellow employed doctors if they used compensation formulas that are different for each doctor. This type of variance would also place both of you at risk of penalties for breaking federal laws regarding physician compensation.

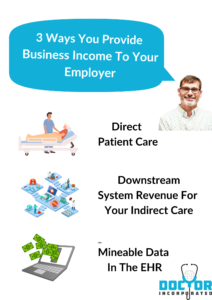

Before leaving fair market value compensation I believe it’s important to note that $/wRVU or your base salary + productivity bonus structure must fall within an industry based $$ range. The wRVU values and compensation range are determined by CMS and various 3rd party agencies like MGMA. The federally compliant range has a floor and a ceiling. From here, your employer plays the arbitrage game with you—making it their goal to pay you as close to the floor as possible, and then simultaneously reap from your small business powers closer to the ceiling level in the marketplace (what they charge the patients & insurance companies for your work). As the following graphic demonstrates direct patient care is just 1 of 3 ways that they make money from you:

So with all this in mind, the first discussion about increasing your compensation with your employer will circulate around steps you can take to make you more productive and efficient including the standard mantra of “just adding one more patient per day.” They will remind you this is the foundational behavioral element of every productivity model—it incentives growing your workload. In the end, the more work you do for them within the same overhead structure, the more revenue you will generate for them from all three sources. Thus, they will ALWAYS encourage you to do more.

You can increase your income through this process, but ultimately your workload in your primary job does have a productivity ceiling, so wedging more work through your work week has its limitations—especially in regards to your time and energy.

Your Employer’s Side Job Menu

In anticipation of this conundrum, your employer will gladly create a menu of extra income options that will allow them to pay you more in exchange for additional services that you can perform for their corporation. These can include things like productivity bonuses, quality bonuses, medical directorships, mid-level supervision, hospital call, medical education, research, leadership-governance roles, etc… Each of these additional opportunities will increase your earned income through your employer, and will typically be ADDED to your current patient care workload.

Your employer is incentivized to provide these options and opportunities to you because it is just another way for them to squeeze more revenue out of your small business powers. Because you are a living-walking micro-business—they can monetize everything you touch and manage—since you are the backbone to their entire medical business operations—pretty much everything from payers flows through you. Again, the arbitrage of this for them is buying low for your services (your pay) and selling high to the 3rd party payers. Yep-you are just like a piece of machinery in their business enterprise—a costly asset that they will seek to generate the maximum revenue through in every possible way—from primary jobs to side jobs.

The route of growing income by working within the employer’s safe harbor is what most will do to address the financial needs of your home. It’s convenient and simply channels the additional income through your current paycheck. This aligns nicely with the mindset associated with choosing employment in the first place—you have no responsibilities to manage within a medical small business and your work is converted to a predictable paycheck by a nice person in your employer’s business office.

You go to work and then you get paid. Easy-peasy, just like every factory worker in America. While I won’t go down this tempting rabbit hole right now-watch for an entire blog post on your emerging role as a medical factory worker in the next few months.

For traditional employees, due to your heavy dependence on a single employer, your employer often is your sole source for creating more income. If that employer is unable to meet your growing income needs through your primary job compensation, or through side jobs—-many of you will search for a new job with a different employer. On average 50% of doctors do this every 3-5 years. It is all part of the physician labor cycle, and it’s why employers are fixated on recruitment and retention strategies for doctors. Physician vacancies are very costly to their enterprise—due to your enormous business power.

Warning to W-2 Workers

Autonomy

Although it’s certainly convenient and less complex-choosing a single employer to be the sole income channel for your household, will place you at risk to become increasingly dependent on that employer. That dependence will only intensify over time because the financial architecture of your home will be completely tied to that source—and making any changes to the relationship can result in extreme disruptions to you and your family. No one likes having their lifestyle messed with, especially doctor families who long for stability after years of migratory training. This is one element of the burnout formula for doctors—whereby you can feel trapped in your job—unable to make changes—while your professional autonomy slowly fades under the control of your employer. You fear the disruptive changes for your family and may even lack the financial reserves to make a change due to your revved up lifestyle. Thus it’s easier to stay and endure the pain—all while the purpose and meaning associated with your job are subterfuged.

Taxes

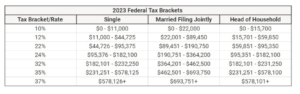

But beyond the loss of autonomy, what many traditionally employed doctors fail to understand is that you are paying up to TWICE as much in taxes as a W-2 employee compared to the 1099 employee (employment lite).

Thus, let me warn you regardless of which employer you work for—if your side job income flows through to you as a W-2 individual tax entity, based on the tiered tax codes, your extra income may not actually net you as much household gain as you think. As you can see from the 2023 individual tax brackets, depending on your income level, you will get less than 2/3 of that money into your home.

A Better Way

In contrast, professional micro-corporations provide many more options for you to reduce the tax burden of your extra earnings through your side job(s). Using this business structure for your side income could allow you to keep nearly all of your earnings.

If we are talking about $40,000 in side job income, we are talking about you keeping $13-14,000 more of your earnings. This is not chump change!

So when you make the extra effort to work harder, I suggest you add to this the mindset of working smarter, not just harder.

The key idea is to receive your side job earnings as 1099 income rather than as W-2 income. In other words, receive it as a contractor designated as an individual/business as noted on the W-9 tax form that whoever is paying you will need. To learn more about the W-9 form, you can check out last week’s blog where I walk through it.

Stating it a different way, you should ask for a W-9 tax form from your side job payer, rather than a W-2 form. This means you will be an independent contractor, not an employee and your compensation will be received as 1099 income.

W-2 Workers Have Options

Before moving on, let me point out that you CAN simultaneously work as a W-2 worker for a corporation as your primary job, AND work as a 1099 worker-side job with that same employer. Your primary job and side job can be separated because the large corporate enterprise that you work for has a broad corporate structure that can support both options. For example, my primary job compensation is paid by the physician network department, and my hospital call compensation is paid by the acute care hospital department. Technically separate sources and separate contractual agreements, but both sources operate under the same parent company. In the purest sense, the dollars you are paid come out of separate profit/loss ledgers from these sources—thus the contractual arrangements & compensation for your professional services (primary job and side job(s)) can be separated into both W-2 and 1099 income.

If you are traditionally employed, it is important that you know this is an option. Most employers are not going to think you are savvy enough to do this, instead, they will default to routing it through as W-2 income.

Now if you are traditionally employed by one corporation, and your side job is with an entirely separate medical corporation, then it’s a bit easier to politely request that you be paid to you as a 1099 worker rather than W-2. Most corporations hiring doctors for side jobs understand the nature of this distinction and are fine with paying you as an independent contractor. (it saves them $ on payroll taxes).

You Are A Business

Independent contractors are small business owners, and they have multiple options for organizing themselves within this designation. In a prior blog post, I covered how most doctors in this situation will choose to be sole proprietors or professional micro-corporation. Business owners as sole proprietors or professional micro-corporations have more diverse and sophisticated options for meeting their growing household needs.

Much like your traditionally employed peers, you can earn more money through extra work through your primary employer. In the end, the extra income ends up being even more financially beneficial when both your primary work and your side work all flow through individual small business structures because your household will get to hold onto more of these earned dollars.

However, as I previously stated don’t resign yourself to missing out on the 1099 boat, if you are traditionally employed and your side job work is with the same employer. You can separate the dual primary job and side job income into W-2 and 1099 sources. You can simultaneously be both an employee and an independent contractor the same large corporate employer.

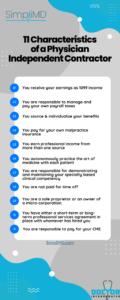

Check out this blog on how to best prepare yourself to be called a 1099 worker, and look over this pictograph covering the characteristics of independent contractors.

One of the nice features about splitting out W-2 and 1099 income with the same employer is that your employee benefits, malpractice, & CME are all covered within your W-2 agreement with that employer—thus you don’t really have to separately source them—like most independent contractors.

But beyond retaining more of your side job income as a non-W-2 worker, working as an independent contractor via a professional micro-corporation can more aptly increase the diversity of income sources that will help meet your household needs.

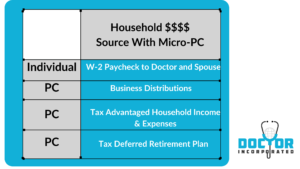

This diversity is a strength for small businesses and, ultimately, reduces your interdependence on a single source of income. Within this professional micro-corporation business model, your household dollars can grow efficiently through three separate income sources: retained, active, and passive income.

Time Is Precious

As you consider these income sources and how they increase your financial position, I would encourage you to reflect on which opportunity(s) will require more of your time or physical presence. In the end, choosing sources that conserve your time is probably your most important consideration. These are typically called passive income options which differ from active income like side work—because you don’t have to be present to earn the income.

I believe the most valuable type is retained income because it involves smart structuring of your active income cash flow that is translated into a tax-efficient accelerant of your net worth. I like it best because it will not cause more work, or take more of your time, but the result is keeping more of your money.

This ties back into the whole reason many doctors take on side jobs, and that is to make more money. That’s the beauty of retained income—no extra work, but you keep 10-15% of your earnings within your household. This can be quite confounding to doctors who are so wired to work hard, and who can only visualize the space of “work more, earn more”. Thus they miss the “work smarter, keep more” opportunity associated with retained income. The former takes more of your precious time, but the latter does not.

Choosing to value time over money is a mindset that each of you should consider.

I like how Warren Buffet states this idea when he says,

“The rich invest in time, and the poor invest in money.”

Beyond time considerations for side income, taxes are the biggest issue.

Taxes Are The Issue

Here lies the real problem, due to your income high income, if your side income is not structured properly, you are only going to add to your tax drag with the extra income.

When it comes to earning side income as a physician, there are several ways to structure how to best receive that income—each with its own advantages and disadvantages.

In this comparison, we will contrast the tax implications of earning $40,000 in side income as a W-2 employee, a sole proprietor, and a professional micro-corporation taxed as an S-corporation (my personal favorite).

W-2 Income

-

W-2 Tax Payer: If you earn $40,000 in side income as a W-2 employee, it will be considered additional wages, and you will receive a W-2 form from the employer. The employer will withhold income taxes, Social Security, and Medicare taxes from your paycheck. Additionally, the employer will also pay the employer’s share of Social Security and Medicare taxes.

As a W-2 employee, you cannot deduct any expenses related to their side income, and you will pay income tax on the full $40,000. The tax rate will depend on their total income and tax bracket, which may increase due to the additional income.

1099 Income As A Sole Proprietor

-

Sole Proprietor: As a sole proprietor, you will report the $40,000 in side income on your personal tax return using a Schedule C form. You will be responsible for paying self-employment taxes, which include both the employee and employer shares of Social Security and Medicare taxes. The self-employment tax rate is currently 15.3% on the first $142,800 of net income.

You may deduct business expenses related to the side income, such as home office expenses, travel expenses, and medical equipment purchases. However, you will pay individual income tax on the net income (revenue minus expenses). The tax rate will depend on their total income and tax bracket, which may increase due to the additional side income.

1099 Income As A Professional Micro-Corporation Taxed As An S-Corp

-

S-Corporation: An S-corporation is a type of corporation that is taxed similarly to a partnership, meaning the profits and losses flow through to the individual shareholders’ personal tax returns. If you form a micro-corporation taxed as an S-corporation and earn $40,000 in side income, you will have the power to determine how to best receive that income through your professional micro-corporation. Generally, your options for flowing dollars into your household through your micro-corporation will include the following 4 categories:

You will pay income tax on any W-2 compensation from your micro-corporation, and the corporation will pay the employer’s share of Social Security and Medicare taxes. The remaining profits will be distributed to you as a shareholder as a dividend, which is taxed at a lower rate than regular income tax.

As an S-corporation shareholder, you can also deduct business expenses related to the side income on your personal tax return. However, there are additional administrative and legal requirements for maintaining an S-corporation, such as filing annual reports and holding shareholder meetings.

Summary

In summary, the tax implications of earning $40,000 in side income as a physician will depend on your business structure or lack thereof.

As a W-2 employee, you cannot deduct any expenses and you will pay income tax on the full amount. As a sole proprietor, you can deduct business expenses but will pay self-employment taxes on the net income.

Finally, as an S-corporation shareholder, you can also deduct business expenses, you will have multiple channels for getting the dollars into your household including dividends that are taxed at a lower rate, but you will have additional legal and administrative requirements & expenses.

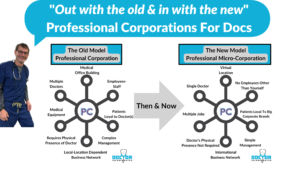

Myths About Professional Micro-Corporations

There are many misconceptions among physicians about how much time and money it takes to own and operate a professional micro-corporation. Let’s just say that is more fiction and urban legend than truth—and that is because doctors falsely assume a micro-corporation is the same thing as private practice.

The truth is that it’s not a private practice, instead it’s a virtual corporation that envelopes you individually. A simplistic way to view it as a business avatar that reflects you personally.

It’s time for this truth to be exposed.

Out with the old and in with the new.

The reality is that it cost less than a vacation you can form a professional micro-corporation and then for a much smaller amount you can outsource its management and operation to an agency like SimpliMD. Or you can choose to manage it yourself via a host of web-based small business companies like Quickbooks and Turbo Tax. By the way, the costs are deductible business expenses.

The tax savings in this setup will easily lead to an incredible return on your small investment, and this will be additive over the years. Not doing this cost me a million dollars in my first 10-15 years of practice.

You Have Been Brainwashed

The first obstacle to overcoming this myth is found within your brain. You have been brainwashed by the corporate propaganda machine that is propagated by medical schools (big corporations) that you can longer be a small business among a sea of large corporations that own medicine. This concept is predicated on the private practice model whose principles and business model are distinctly different than the professional micro-corporation.

The professional micro-corporation doesn’t compete with large corporations, or even small corporations but instead is a virtual entity that surrounds you individually. Within any job or work structure, you can configure for individual physicians, your professional micro-corporation can be layered into.

Let me help you visualize what this can look like in the two most common job structures that you could find yourself within Traditional employment and group practice/partnership in private practice.

Frankly, most of you miss this due to your assumptions about what is possible. It just takes a little innovative thinking to you see employment lite and a professional micro-corporation embedded in a group partnership. Check out how it looks:

Your first step to embracing this involves understanding that you have a special power to incorporate, then you have to begin to see yourself and your professional service work as a micro-corporation. The truth is that you are a business.

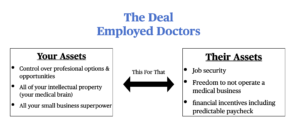

When doctors organize and operate as a business, they thrive. When they subjugate their small business powers to the large corporations through what I call “the deal”, they set themself up for burnout as employees.

This is what the unwritten deal looked like when you signed up to be a traditional employee.

While some doctors can thrive as employees of large corporations, most can’t. That’s because doctors need professional autonomy and cold truth is that traditional employment erodes your autonomy.

Next week I am going to unpack further the tax elements of side jobs and break down how $40,000 of side income flows through the W-2 and 1099 taxable entities. It will help you discover how you can keep every one of those side income dollars.

[/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section]