{kind=link}

[et_pb_section fb_built=”1″ _builder_version=”4.16″ global_colors_info=”{}” theme_builder_area=”post_content”][et_pb_row _builder_version=”4.16″ background_size=”initial” background_position=”top_left” background_repeat=”repeat” global_colors_info=”{}” theme_builder_area=”post_content”][et_pb_column type=”4_4″ _builder_version=”4.16″ custom_padding=”|||” global_colors_info=”{}” custom_padding__hover=”|||” theme_builder_area=”post_content”][et_pb_text _builder_version=”4.19.1″ background_size=”initial” background_position=”top_left” background_repeat=”repeat” hover_enabled=”0″ global_colors_info=”{}” theme_builder_area=”post_content” sticky_enabled=”0″]

I get it, receiving a large paycheck on a regular basis feels great!

Predictable Pay

One of the most appealing features for a doctor becoming a traditional W-2 employee of a large corporation is receiving a predictable paycheck that is regularly deposited into their bank account. By the time it gets there, it has been filtered and washed from all local, state, and federal taxes. This includes accounting for all the benefits that are paid for you (in reality you and your employer share these costs), and if you are wise, you have your payment system set to max out your tax-advantaged retirement funding through your 401(k), 403(b) and the like. After all this process is completed, the dollars that land in your bank is yours to spend, save, or give as you want.

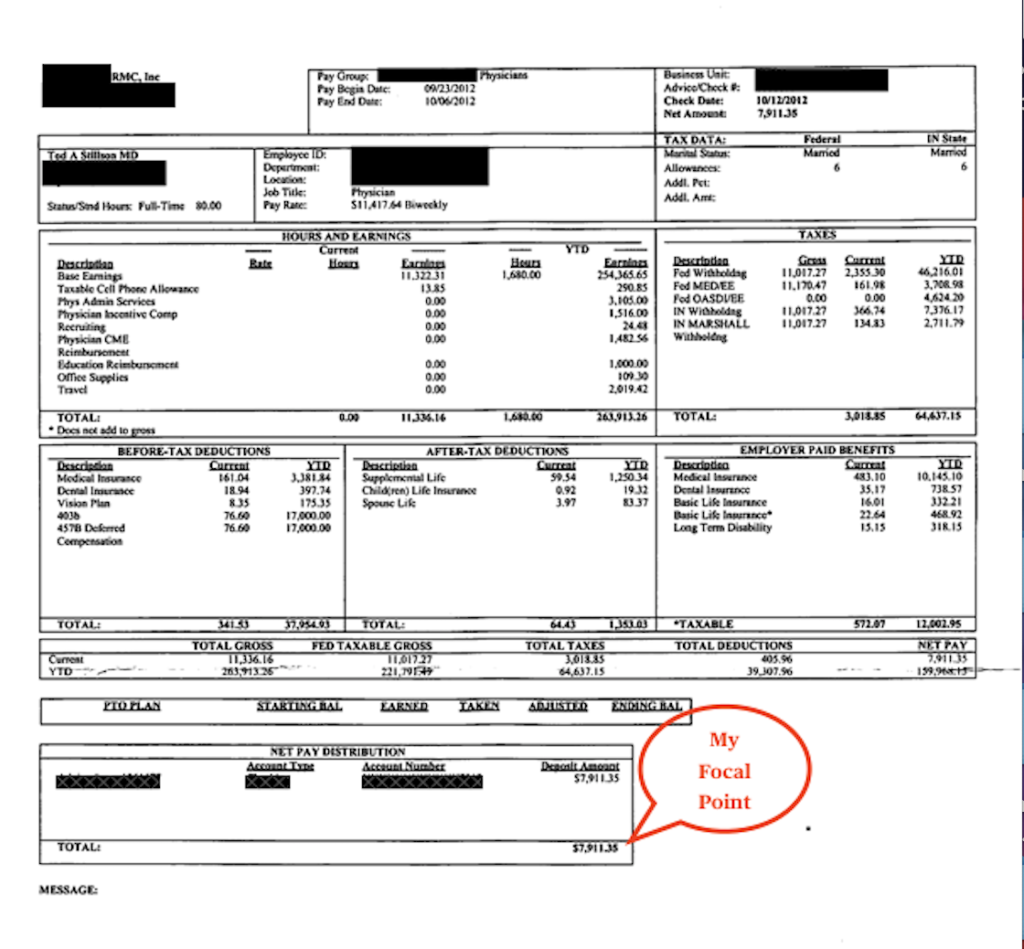

The autonomy and pleasure of having a job associated with a high income are fantastic on many levels, and the simplicity of receiving such a large sum of money regularly without the hassles of running a business is a pretty good deal. I did this same W-2 employee process for years, and blindly enjoyed the ease of placing things on auto-pilot while watching to make sure the money made it to my account. I always said to myself, “I can’t believe I make this much money doing something I love”. Through large corporate employment, I enjoyed simply practicing medicine, getting fair market value compensation, and eliminating the hassles of managing a small medical business. This is what my paycheck looked like in 2012,

Take Home Pay Focus

Like most of you, my singular focal point was the bottom-line take-home pay. The rest of my paycheck was a lot of blah-blah-blah worthy of being ignored or glossed over at a minimum. I mean who really wants to observe the pain of how much you are paying in taxes with each pay period?

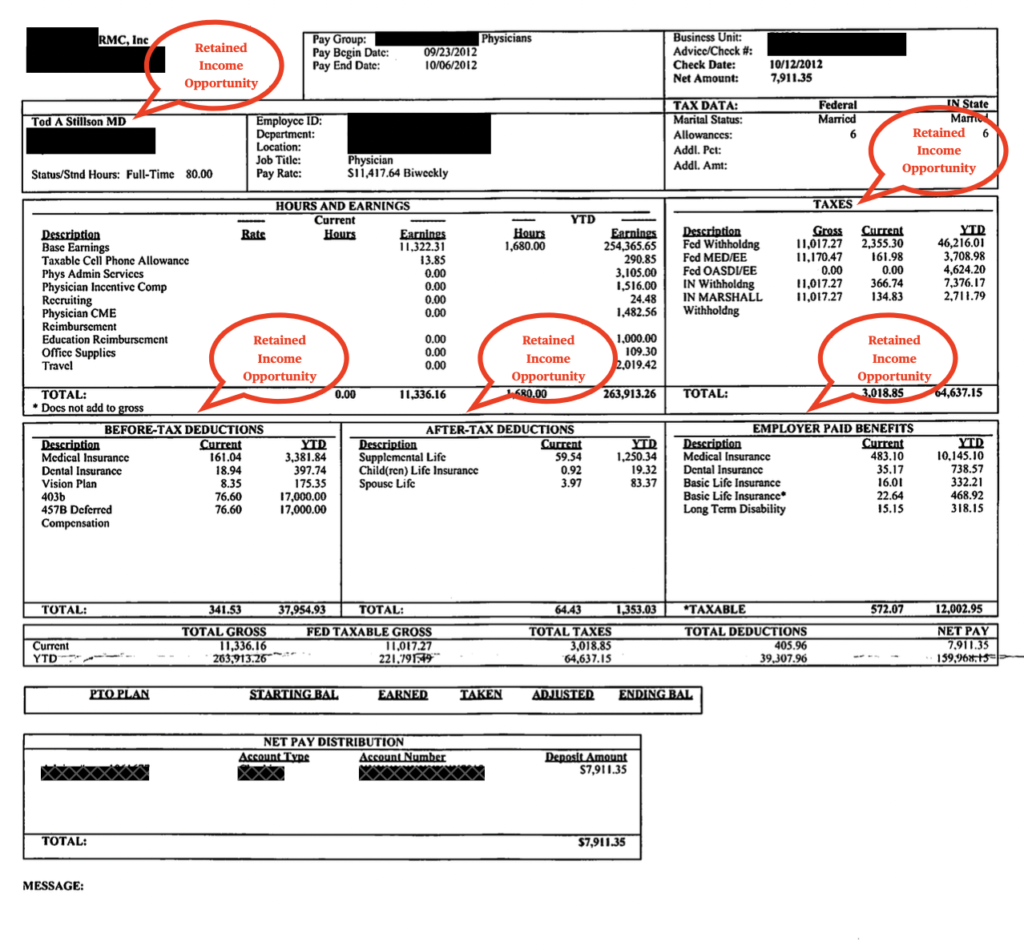

The Invisible Opportunity

Fast forward to the present day and quite honestly most of you never even see your paycheck. The digital age has ushered in the direct deposit into your bank account that basically bypasses a paycheck, pays stub, or any physical evidence of what happens between the dollars you earn, and the dollars that you actually receive. Therefore, many of you may be unaware of what this looks like, and probably don’t care much about all the filters demonstrated in this paycheck example. The dollar amount that you are paid is so high, that rest just “is what it is.”

But, you should really pay attention, because the average high-income W-2 employee is losing about 10-15% of their earned dollars in this W-2 bath. As I will explain, by starting your own micro-PC and then converting your traditional employment to a PC-employment lite structure, you will regain control of your hard-earned dollars. Then as the money is directed through your PC first, rather than to you individually, you have the power to manage those dollars as they traverse through the various filters of a paycheck. Here are where the opportunities to retain income are found in the paycheck of every traditionally employed doctor:

Each of these retained income opportunities is opened up by starting your own micro-PC and then converting to a PC-employment lite structure with your employer. This is the first and most important mind shift decision that every employed doctor must make. This doesn’t mean you are “going into private practice”, but what does mean is that you are covering yourself individually in a micro-PC wrapping and then continuing to work for your large corporate employer with the exact same compensation structure as you did as a traditional employee. You still have no responsibilities to manage the clinic, your clinical operations, etc… Honestly, pretty much everything remains the same, except you now are responsible to source and managing your benefit plans (which is better because you can individualize them) and now you can fully control the flow of your dollars earned. This all happens by adding “PC” to the end of your name. This leads to your compensation flowing to your micro-small business first rather than to you individually. From a tax standpoint, this puts you back in control of your earnings and makes a huge difference as I will explain below.

The Small Business Cash Flow To your Home

As a small business person, your household dollars will now flow to you in a different way than you are used to as a traditional W-2 employed physician.

You will still be paid a W-2 salary, but this time your own business will be paying you a “reasonable salary”. But unlike the traditional employee, as a micro-PC owner, you will have multiple cash flow channels into your home. Thus your self-employed W-2 salary from your own company will not need to be the equivalent of your salary as a traditional W-2 employee of a large corporation. In fact, as I will explain, less W-2 compensation is better in regard to your taxes.

In fact, by lowering your self-employed W-2 salary and following the S-corp safe harbor ratio of 60-40 you will be able to reduce the tax burden associated with your high income. 60-40 reflects S-corp owners receiving 60% of their income via salary, and 40% of it via corporate distributions. Let me take you on a short primer on how a PC-employment lite arrangement will lead to tax savings for you compared to receiving all of this income in one lump sum as traditional W-2 employed doctors do.

Taxes You Pay on S Corporation Salary and Payroll Earnings

S Corporations must have payroll and salaried employees. Even if you’re running the business by yourself or with a spouse, you will still need to run payroll and deal with payroll taxes.

You will pay several types of tax on any payroll amounts that you pay to employees or business owners:

- Employer payroll tax of 7.65 percent on payroll amounts earned

- Employee payroll tax of 7.65 percent on payroll amounts earned

- Federal income tax on payroll amounts earned after a standard deduction

- State income tax on payroll amounts earned after a state deduction

- Unemployment taxes payable to the IRS (FUTA) and your state (SUTA)

Taxes You Pay on S Corporation Distributions

Money that you don’t take out of your business as payroll can later be taken out for you as a distribution.

When you make a distribution from an S Corporation, anyone receiving a distribution will pay taxes as follows:

- Federal income tax on money distributed

- State income tax on money distributed

The biggest difference, and the advantage of being taxed as an S Corporation, is that you won’t pay self-employment or payroll tax on the distributions. This saves you a total of 15.3 percent of what you pay out as a distribution versus receiving it as W-2 income as an owner.

Multiple HOusehold Dollar Sources

So on top of your PC’s self-employment salary to yourself, along with any salaried income that is associated with employed family members (there are many tax benefits to employing family members), your PC will provide dollars into your household via 4 other general sources:

- PC Distributions ( profits)-for tax purposes distributions are usually better than bonus compensation because bonuses must be run through payroll (taxes) and distributions are not taxable.

- Tax-advantaged household income as a dwelling unit reimbursement program.

- Reimbursement for business expenses that are shared within your household.

- Tax-deferred retirement plans like a solo 401 (K) or cash balance plan. These can be as much as 3x larger than ERISA-capped plans from large employers as traditional W-2 employees.

In this small business model, the total cash flow into your household will be much less predictable compared to a traditional W-2 employee. For some that make this arrangement a bit more challenging as you attempt to mirror your household expenses. That is because as a small business owner, the dollars arrive in your bank account in a more asynchronous pattern., which takes a little getting used to.

I would also add that the most significant tax-advantaged financial benefits for high-earning small business owners occur within your retirement account, These are dollars you won’t be spending now, so although end up in your household as a large amount of retained income, those dollars will not be available to pay for your current spending. However, when the cash flow in your micro-PC is constructed properly you will have the same amount of dollars in your bank account to spend as the traditionally employed doctor’s take-home pay. But the key difference from traditional employment is that you will pay far fewer taxes and have a significantly larger retirement account as a micro-PC owner. Both of these elements of paying fewer taxes and growing your retirement account will allow your high income earnings to be translated into the more rapid growth of your net worth.

Your self-employment (along with any employed family members) will result in a consistent paycheck (weekly, biweekly, or monthly whichever you prefer). You can even automate this as a direct deposit and enjoy the pleasure of seeing the money land in your bank account after the earned dollars have been rinsed off all of their federal, state, and local tax obligations. Whatever payroll system you set up will do this for you.

But the rest of the money in your small business’s bank account will flow through a series of reimbursements, invoices, and distributions that will also land in your household, but in a more tax-advantaged manner. The net effect is that you be able to retain 10-15% more of your earned income over a calendar year. However, this asynchronous cash flow will require you to more actively manage your household expenditures to match the irregular flow of dollars into your home.

Lowering your Tax bill

In this micro-PC model, your predictable salaried paycheck will likely be less than you are used to receiving as a traditionally employed W-2 physician. This is good because it is an important strategy associated with lowering the effective tax rate on the dollars that you earn.

In order to know how much your self-employment payroll needs to be set at, it is helpful to know your household expenditures for each month and even more ideally organize and follow an annual household budget. All of this will allow for a reverse engineering calculation by your accounting service to help you determine your minimum salary after they take into account the 4 other sources of dollars that will flow into your home. The accounting service assisting you with payroll will need to know the following information to determine this self-employment salary:

- An understanding of the IRS-defined “reasonable” salary range for your occupation.

- Determine how you want to manage charitable giving:

- Do you want it to come out of your PC as a business expense?

- Do you want it to come out of your personal funds which are less tax-advantaged at your high Income due to Alternative Minimum Tax (AMT) rules

- Determine your savings rate that includes your retirement funds and your automated(hopefully) personal investment plan. I suggest that 20-30% of your gross income should be saved if you can afford it.

- Determine what is your needed monthly income to meet your budget (aka spending plan) that includes the above elements. If this is new to you, I recommend either Mint or Every Dollar for doing this.

All of this will add up to determine the monthly W-2 compensation that is needed to meet your minimum needed monthly expenditures.

Predictable Household Dollars for the PC owner

From a predictability standpoint, each month you will receive dollars in your bank account from your small business from two sources:

- You and any family members on the payroll

- Your tax-advantaged household income such as a dwelling unit rental

Corporate distributions to owners are typically made annually, based on the financial performance of the small business. This number can be relatively predictable each year, based on the professional arrangements and contracts that you engage in through your micro-PC. But as previously stated, and I will restate due to its importance, an S corp distribution is note is not subject to Social Security or Medicare taxes. This means distribution will provide significant tax savings in comparison to receiving it in your household via payroll only (like a traditionally employed physician).

This is one of the many ways that S Corporations can be great way to reduce the amount of tax that you pay as a business owner.

In summary as a high-income earning physician, your earned dollars are easy targets for the IRS through your W-2 earnings, as I have written about in KevinMD. So although the predictable direct deposit in your bank account is nice, you are losing 10-15% of your earnings in this process. If you form a micro-PC and then use that in a PC-employment lite arrangement you can continue to work for a large employer but now you gain control over your earnings as a micro-PC business owner. This will give you control over the flow of your earned dollars and thus you can retain a significant amount of those earnings. In addition to reimbursements, tax-advantaged household income, and retirement funding–the largest amount of your household dollars will arrive from your micro-PC via a two tax-advantaged channels(the 60:40 S Corp safe harbor previously mentioned):

- By paying yourself a “reasonable” W-2 salary

- By taking money out as a distribution, based on your own in the company

It’s the difference between your salary amount and your distribution amount, which reduces the amount of tax that you will owe. The net effect of all of this is a lower effective tax rate for your household, fewer total tax dollars paid annually, and more money that is retained in your home. All of this adds up faster-growing net worth, and ultimately an early arrival at financial independence much faster than your traditionally employed physician peers.

Thus choosing to start your own micro-PC and then using it within a PC-employment lite structure is the smart move for any physician! And that is exactly what I have done.

[/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section]