{kind=link}

[et_pb_section fb_built=”1″ theme_builder_area=”post_content” _builder_version=”4.21.0″ _module_preset=”default”][et_pb_row _builder_version=”4.21.0″ _module_preset=”default” theme_builder_area=”post_content”][et_pb_column _builder_version=”4.21.0″ _module_preset=”default” type=”4_4″ theme_builder_area=”post_content”][et_pb_text _builder_version=”4.21.0″ _module_preset=”default” theme_builder_area=”post_content”]

How Much Should You Pay Yourself?

What Is The Value Of Your Services?

In my last post, I discussed the importance of getting paid what you are worth. This is a critical concept to understand whether you are an employee, or whether you are self-employed as a small business owner/ independent contractor. Knowing the value of your professional services to others is an essential feature of negotiating a fair-market-value contract.

How Much To Pay Yourself?

In response to my post, a self-employed physician from California asked the question:

What if you own the business and pay yourself?

This is a fantastic question whether you are in traditional private practice, or a single-member professional corporation. Each of the small business owners has to decide how much to pay themself.

I am going to answer this self-employed doctor’s question from the perspective of the single-member professional corporation owner who is working as an independent contractor in a primary job via what is called an employment lite agreement. It’s what I do, so I can speak to it from a personal perspective.

Your Professional Micro-Corporation Will Be Paid

First, understand that your compensation for your professional services will be paid to your professional corporation in this contractual arrangement. The value of that compensation is essentially the same whether you are employed or a contractor. Also, understand that the total value is not just the salary/comp formula but also includes benefits and professional fees.

Put another way the labor expenses for employed doctors include their salary/compensation formula + benefits +retirement contributions +professional fees like malpractice insurance. This represents your total value and expense to your employer.

When you either start with a fresh employment lite agreement or convert from a traditional employee to an employment lite agreement it is important to know that your professional micro-corporation should be paid the equivalent total fair market total value labor expense as the employed doctor. This “grossed up” number is important because your micro-corporation will be responsible to pay for your retirement, benefits, and professional fees like malpractice insurance.

In the end, what an employer pays you for your professional services should be the same whether you have a traditional employment contract or an employment lite contract. Locums are a whole different thing and will cost employers more than both of these contractual arrangements.

Much like a traditional employee, you will want to maximize the Fair Market Value of your employment lite contract—which was the point of my last post. I encourage you to reach out to Contract Diagnostics to complete their Compensation Rx for only $297 to find out your true value.

As a professional micro-business owner, you may also have additional side job incomes that contribute to your primary job compensation. Just like any small business, generating revenue is a critical feature of a healthy business and therefore having diversified revenue sources/contracts is always helpful.

How Much Should You Pay Yourself?

For the single-member professional micro-corporation owner, once you have a relatively predictable value for your annual corporate revenue (based on FMV contracts), this is where the fun begins—especially if you are a high-income earner like a doctor.

This is one of the elements that sets you apart from the rest of the single-member small business owners in America—their income can be less predictable and they are always working towards stabilizing and growing their revenue. As a physician, your professional micro-corporation has a very predictable high revenue based on your FMV contract, but it also lacks scalability due to it being a single-member corporation that is completely dependent on you alone. In the end, you as an individual doctor can only do so much work. Therefore your professional corporation will usually have a ceiling on its potential revenue.

Savvy doctors who really begin to understand their business powers will use their high income, professional skills & earned assets to create an enterprise of active and passive income sources and businesses that eventually create additional income sources—that don’t require your time or presence—and thus brake the scalability barrier of your micro-corporation. In essence, they will master how to make their money work for them. This is why my enterprise is made up of 9 businesses and not just my PC.

The Fun

The “fun” for the self-employed physician in his/her single-member corporation is figuring out how to get as much of your earnings/corporate revenue into your household in the most tax-efficient manner. Unlike your traditionally employed peers whose earnings are filtered through the highly taxed W-2 channel—you have options.

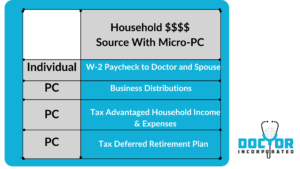

As a micro-corporation owner, your household income will arrive to you via 4 basic channels as noted below.

You will note your salary is just one of those 4 channels. It is typically the largest of the 4 and thus it is the most important —and the good news is that you get to decide the amount!

I can’t over-emphasize this 4 channel concept enough to you:

small business owners understand all 4 of these cash flow channels and use each to wisely get dollars into their homes in the most tax-advantaged manner.

Your paycheck is just one of the sources of these dollars to your household.

This is in contrast to traditional employees, whose paycheck and ERISA-limited retirement contributions reflect the total household value of their work. Typically these doctors pay a much larger percentage of their earnings to taxes than self-employed doctors.

Reverse Engineering

Because the earnings for your PC are relatively predictable based on FMV, you have the power to determine your salary and the dollar value of the other sources of household money—through what I call a reverse engineering process.

The reverse engineering process requires you to know two important numbers:

-

Your annual household expenses/spending. Although I believe in budgets, at a minimum every doctor should know how much they are spending each year-including all loan and credit card payments. This number is the minimum value that you should set your salary at.

-

Your IRS-compliant lowest “reasonable salary”. This represents the range of income that the IRS expects a doctor in your specialty to make each year. If you pay yourself less than this amount, the IRS is more likely to audit you out of concern that you are trying to evade taxes. The “sweet spot” for lowering your taxes as a doctor is to keep your reasonable salary as low as possible.

As a self-employed doctor, understanding the concept of a “reasonable salary” defined by the IRS can significantly impact your tax liabilities. By ensuring that you are paying yourself the lowest reasonable salary, you can effectively lower your payroll taxes and maximize your business’s financial potential.

The IRS has specific guidelines in place to determine what constitutes a reasonable salary for self-employed individuals, including doctors. This determination takes into account factors such as the nature of your medical practice, your level of experience and expertise, industry standards, and the amount of time and effort you dedicate to your business.

By adhering to these guidelines and paying yourself a reasonable salary, you can demonstrate to the IRS that you are not attempting to evade taxes or artificially reduce your income. This not only helps you stay compliant with tax regulations but also provides solid documentation in case of an audit.

The reverse engineering process also ideally should include an evaluation of which tax entity for your professional corporation will provide your household with the maximum tax-advantaged dollars in each of the 4 channels.

Let me emphasize this is highly individualized for every doctor—and includes multiple factors including specialty, income, fringe benefit needs, family structure, assets, and other passive/active income. The complexity of this is why I recommend an agency like SimpliMD help you with this process—they have a team of legal, accounting, and business professionals who can provide you with an objective analysis of this for a reasonable fee. This What-If Tax planning worksheet provides extremely valuable data in a side-by-side analysis like this example.

You can schedule a free business coaching meeting with them here to begin exploring this.

For the sake of simplicity, let me walk you through some of the general concepts within the framework of an S-Corp vs a C-Corp for your professional micro-corporation.

Most doctors as single-member professional corporations will choose S-Corp taxation, but again this is very individualized and worth of analysis with a reputable agency like SimpliMD.

Physician Self-Employed Salary in Their Micro-Corporation: S Corp vs. C Corp

When establishing a micro-corporation as a self-employed physician, choosing the right corporate structure is crucial. The decision between an S corporation (S corp) and a C corporation (C corp) can have significant implications for how you pay yourself a salary. I am going to explore the differences between these two structures and discuss how they affect the determination of your salary as a self-employed physician.

-

Understanding the S Corporation (S Corp): An S corporation is a pass-through entity that allows profits and losses to flow directly to the shareholders’ personal tax returns. In an S corp, the owners, known as shareholders, can pay themselves a reasonable salary as employees and receive additional income through distributions. These distributions are generally not subject to self-employment taxes, providing potential tax advantages.

-

The C Corporation (C Corp) Option: A C corporation is a separate legal entity responsible for its taxes and liabilities. As a self-employed physician operating as a C corp, you would become an employee of the corporation. This means you would receive a salary, subject to income tax and payroll taxes, including Social Security and Medicare taxes. Any profits retained within the corporation are taxed at the corporate level. When distributing profits to shareholders, they may be subject to additional taxes, such as qualified dividend rates.

-

Salary Determination for S Corporations: In an S corp, the IRS requires that shareholders who provide services to the corporation receive “reasonable compensation” for their work. The salary should be commensurate with the services provided and comparable to what a non-owner employee in a similar role would earn. Setting an unreasonably low salary and distributing most of the profits as dividends may attract scrutiny from the IRS. A reasonable salary helps ensure compliance and reduces the risk of audits.

-

Salary Determination for C Corporations: As an employee of a C corp, your salary would be determined based on industry standards, your qualifications, and the specific services you provide. Unlike an S corp, there is no requirement for the salary to be “reasonable” in relation to the work performed. However, it is essential to ensure that the salary is justifiable and aligned with market rates to avoid potential tax issues or challenges in the event of an IRS audit.

-

Tax Considerations: Both S corporations and C corporations have distinct tax considerations. In an S corp, the portion of profits distributed as dividends to shareholders is generally not subject to self-employment taxes. This means potential savings on Social Security and Medicare taxes. However, the salary portion is subject to payroll taxes.

In a C corp, both salary and dividends are subject to taxes. The salary portion is subject to income tax and payroll taxes, including Social Security and Medicare taxes. Dividends received by shareholders are subject to taxation at the individual level, potentially at qualified dividend rates.

It’s important to consult with a tax professional or accountant specializing in physician finances to ensure compliance with tax laws and make informed decisions about your salary and overall tax strategy.

The 60/40 Rule

An important concept that is used for a physician who owns a single-member professional corporation taxed as an S-Corp is the 60/40 rule. This rule, which refers to the allocation of income between salary and distributions, can significantly impact your tax obligations and overall profitability.

The 60/40 rule states that as a physician S-Corp owner, you should allocate at least 60% of your PC’s revenue as a reasonable salary and no more than 40% as distributions. This allocation is based on the IRS guidelines aimed at preventing excessive tax avoidance through misclassification of income.

By adhering to this rule, you can ensure that you are properly compensating yourself for the services you provide while minimizing your tax liability. Allocating a reasonable salary demonstrates that you are paying yourself in line with industry standards and avoids potential audits or penalties from the IRS.

Moreover, following the 60/40 rule allows you to take advantage of potential tax savings. By keeping a portion of your income as distributions, which are subject to lower self-employment taxes compared to salaries, you can optimize your overall tax burden.

It is important to note that every physician’s situation may differ based on factors such as specialty, location, practice size, and personal financial goals. Consulting with a qualified accountant or financial advisor who specializes in physician S-Corps can provide valuable guidance tailored to your specific circumstances.

Understanding and implementing the 60/40 rule is essential for physician S-Corp owners seeking financial success. By appropriately allocating income between salary and distributions, you can ensure compliance with IRS guidelines while maximizing tax savings. Seek professional advice to navigate this complex area effectively and make informed decisions regarding your finances.

Example

If you were a physician currently earning $500,000 as a traditional employee you would pay W-2 taxes on all of that $500,000 income minus any itemized deductions.

If your PC was paid that same $500,000 (assume for the sake of this example that the benefits, professional expenses, and retirement costs are the cost neutral for both doctors), this doctor’s household income would arrive via:

-

60% Salary: $300,000 as W-2 income

-

40% Business Channels

-

Tax Advantaged Household Income/Expenses: $80,000

-

Tax Deferred Retirement Plan: $70,000

-

Business Distributions: $50,000

-

The W-2 tax burden for the physician as a professional micro-corporation will be significantly less than if they chose to be a traditional employee with only $300,000 being subjected to payroll taxes versus $500,000.

And in the end, the 4 channels of cash flow into dollars for the doctor as a professional micro-corporation will result in a 10-15% retention of the earnings in comparison to the traditional employee.

Summary

Determining your salary as a self-employed physician involves a thoughtful analysis of your financial health, personal needs, market conditions, long-term goals, and tax entity options. By considering these factors, seeking professional guidance, and continuously evaluating your financial situation, you can establish a fair and sustainable salary structure that aligns with your expertise and aspirations.

Consulting with professionals who specialize in physician finances can provide valuable insights and help you make informed decisions based on your specific circumstances. Ultimately, the choice between an S corp and a C corp should consider both tax implications and the long-term goals of your personal and professional life.

[/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section]