{kind=link}

[et_pb_section fb_built=”1″ theme_builder_area=”post_content” _builder_version=”4.21.0″ _module_preset=”default”][et_pb_row _builder_version=”4.21.0″ _module_preset=”default” theme_builder_area=”post_content”][et_pb_column _builder_version=”4.21.0″ _module_preset=”default” type=”4_4″ theme_builder_area=”post_content”][et_pb_text _builder_version=”4.21.0″ _module_preset=”default” theme_builder_area=”post_content”]

W-2 Physicians are getting slaughtered by taxes and they feel helpless to do anything about it. Sadly this is mostly true, as long as they remain W-2 workers.

But their self-employed peers know that they have access to two small business methods that significantly lower their tax burden:

-

On the income side of the ledger-they keep their self-employed “reasonable” salary at a low level while also receiving tax-advantaged corporate distributions

-

On the expense side of the ledger-they maximize their household advantaged deductible business expenses.

Both steps have the same net effect to lower the taxable adjusted gross income for the self-employed doctor—thus both steps lead to less taxes paid.

The W-2 physician can’t make either of these moves.

Business Expense Deductions

Too many of you are hyperfocused on income and forget the flipside of professional earnings—expenses.

Both offer a path for adding dollars to your household.

A couple of my recent posts addressed the income side:

This post is going to address a relatively hidden subject to many doctors, which is leveraging tax-advantaged business expenses as a way to lower your taxes.

With the physician labor market primarily being populated with employees, the general need to track and leverage business expenses has faded in importance. W-2 employees don’t get to deduct their professional business expenses thus there is little incentive for most of you to understand this subject.

But business expense deductions are a concept that every doctor should be tuned into.

Why? Because you lose a lot of your hard-earned income to taxes every year.

Business deductions are one of the best ways for you to reduce the tax drag on your high income.

Only those of you who receive your income as a non-employee get to access the use of these deductions. Thus if you are exclusively an employed W-2 doctor, you are left out in the cold with this tax play.

There are a number of advantages to being an employee, but taxes are not one of them. Physicians as W-2 employees are among the most heavily taxed citizens within the US, and if you earn >$400,000 it may get worse.

How can you avoid this? By either working full-time or part-time as a non-employee and thus opening the door to business expense deductions.

In contrast to W-2 workers, if you earn your income through your professional micro-corporation or designate yourself as a sole proprietor/single-member LLC, you are allowed to deduct your business expenses. This applies both to your primary job and your side jobs.

When it comes to income—W-2 workers vs Independent Contractors will be relatively equivalent in regard to their fair market value compensation. Still, non-employees will have a slight advantage due to their ability to manage their taxable dollars.

But when it comes to expenses and taxes-non-employee independent contractors have a sizable advantage over W-2 employees.

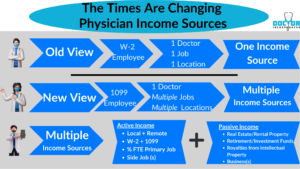

Many of you are starting to become more aware of the tax burden associated with W-2 work, and thus you and your peers are transitioning to full-time or blended non-employee jobs.

With as many as 40% of doctors performing side jobs, it’s common for you to have a combination of W-2 and 1099 income. In fact, as I interact with clients through SimpliMD, I see this more and more frequently—stacking jobs is increasingly normal for the younger generation of doctors.

Thus the importance and value of deductible business expenses are growing among our tribe as more and more of you work as non-employees and provide your professional services as independent contractors.

So let’s take a look a closer look at this subject—because it can save you a lot of money!

Tax Advantages Of Being A Single-Member Business

If you have organized yourself as an individual business—whether that be as a sole proprietor, single-member LLC, or as a professional micro-corporation—you have unique tax opportunities when it comes to business deductions. By understanding and utilizing these deductions effectively, you can maximize your tax savings and ensure you and your micro-corporation operates in the most financially efficient manner possible.

One of the key advantages of being a physician who works as an individual business is the ability to deduct your professional-business expenses. These deductions can include everything from auto-expenses, office supplies, and equipment to professional development courses and even travel expenses related to attending conferences or medical seminars. For instance, my recent CME to Iceland, Ireland, and England was covered by business—and because I went with CME Away by SeaCourses—my spouse was included for FREE.

It is important for a physician who is a business to work closely with knowledgeable tax advisors or accountants who specialize in healthcare professionals. They can provide valuable guidance on which expenses qualify as legitimate business deductions and help navigate the complex world of tax regulations.

Why Schedule C Is Important

Schedule C is an essential component of the U.S. income tax system, particularly for self-employed individuals and small business owners. It is a form that allows taxpayers to report their profits or losses from a business or profession as part of their annual tax return.

For those who are unfamiliar with Schedule C, it serves as a comprehensive record-keeping tool for reporting various aspects of business income and expenses. By completing this form accurately, individuals can ensure compliance with tax regulations while maximizing deductions and minimizing their overall tax liability.

Understanding Schedule C is crucial for anyone engaged in self-employment or operating a small business. It provides a clear framework for documenting revenue sources, deductible expenses, and calculating net profit or loss.

For high-income earners like yourself, it is critical for you to understand the IRS options available to reduce your taxes.

For doing the exact same work, a physician being paid as a W-2 employee will pay significantly more in taxes than the physician who receives it as a 1099 non-employee income. This is all due to being able to use Schedule C on your 1040 individual tax return as a sole proprietor or single-member LLC.

If you are organized as a professional micro-corporation you will get to deduct your business expenses as well—but it will be done with your corporate tax return via forms 1120 or 1120S.

Who Uses Schedule C?

The quick answer to use Schedule C is sole proprietors and single-member LLCs.

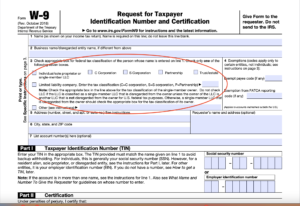

But let me explain a bit more because you will arrive at unlocking schedule C through the use of IRS Form W-9.

If you are receiving your earnings through your business, those earnings are considered non-employee income. You will have to complete a W-9 form for the company paying you for your professional services. This will notify the IRS that your income will be reported by the business entity checked on Form W-9.

It also informs the IRS that the business entity will be making a quarterly tax payment for that income.

This is in contrast to the Form W-4 that employees complete. It is a form used by employers to inform them how much to withhold from your paycheck for your taxes. The IRS makes the employer responsible for this process with employees.

The W-9 Form

The W-9 form serves as a request for taxpayer identification number and certification, enabling businesses to gather necessary information from individuals or entities they engage in financial transactions. If you earn your money as a professional micro-corporation, this form becomes particularly relevant when engaging in professional service agreements (PSAs), receiving payments from insurance providers or government agencies, or conducting business with other entities that require tax reporting.

When you complete this form for your non-employee compensation, you will check the box that indicates which type of business you are as an individual.

When you receive your income as a sole proprietor or single-member corporation, it unlocks Schedule C for your use for the profit and loss of your business.

This special Schedule C space is not accessible to W-2 workers, nor is it accessible to S & C Corps or partnerships.

Schedule C is Valuable To Doctors

Physicians as individual micro-businesses play a crucial role in the healthcare industry, and understanding the importance of Schedule C is essential for these entities. Schedule C is a tax form that allows you to report your business income and expenses as sole proprietors or single-member LLCs. By accurately completing this form, physician micro-corporations can ensure compliance with tax regulations while maximizing their financial benefits.

One of the key reasons why Schedule C is important for physician micro-corporations is that it enables them to claim deductions for business expenses. These deductions can significantly reduce their taxable income, resulting in lower tax liabilities. From office rent and equipment costs to professional fees and marketing expenses, Schedule C allows physicians to deduct various expenditures associated with running their micro-business.

Schedule C plays a vital role in the success of physician micro-corporations. It allows these entities to claim deductions for business expenses, demonstrate profitability, and make informed decisions about their operations.

Differences Between Sole Proprietor & Professional Micro-Corporation Deductions

It is noteworthy that all of this information about Schedule C deductions will be applicable to self-employed doctors who have single-member professional corporations (PC) or professional LLCs (PLLC) taxed as S or C-Corps—however you will not use Schedule C, instead these deductions will be used within your 1120 corporate return.

It is also noteworthy that the tax code for sole proprietors/single-member LLCs and single-member professional micro-corporations taxed as S-Corps or C-Corps are unique and a bit different from another.

Sole proprietors & single member LLCs using Schedule C get access to “basic” tax advantages in terms of professional business expenses. The advantage of this business structure for you is its simplicity. Moreover, they eliminate the need for complex legal formalities expenses, and paperwork associated with other business structures. You only file one integrated tax 1040 tax return and Schedule C represents your business activity that is integrated into your individual taxes.

The bottom line is that sole proprietors & single member LLCs are cheaper and simpler to manage.

In contrast, professional micro-corporations taxed as S-Corp and C-Corps provide additional tax advantages not available to the sole proprietor/single-member LLC. These tax advantages include some “hidden deductions” that only the wealthy know about including robust deductible fringe benefit options. The downside is the larger expense of setting up and operating/maintaining your corporation. Additionally, you will have to complete a corporate tax return on top of your individual 1040 return.

The cost/benefits of which business structure is best is highly individualized and should be done under the direction of a tax professional or accountant. At SimpliMD we are experts in helping physicians sort through these decisions. Our legal department is directed by an attorney with added tax qualifications and works exclusively with doctors. You can reach us here for a free business coaching session: https://calendly.com/drinc/45min

High net-worth individuals have unique business, asset, and fiduciary needs and I advise you to work with professionals who understand you in this context.

Due to your large income, high tax bracket, and the need for asset protection— your best individual business structure will usually be a single-member professional corporation (PC) designated as an S-Corp. This is especially true if you will be earning $40,000 or more through your business. Check out this case study if you want to understand how and why this is best.

Overview of Schedule C

So now, let me break down Schedule C for you and take a closer look at the different sections so you can know what information you will need to provide when you complete this form

Part I – Income

The first part of Schedule C is where you report all of your business income. This includes any money you earned from sales, services, or other sources related to your business. You’ll need to provide a description of the type of income you received, the date you received it, and the amount of money you earned. If you have more than one type of income, you’ll need to report each one separately.

You may also need to include any returns, refunds, or allowances you received for your business. If you received any payments that were not reported on Form 1099, you’ll need to report them on this section of the form as well.

If you have both W-2 and 1099 income, only your 1099 income will be reported here

Part II – Expenses

In this section, you will report your business expenses incurred to run your business like advertising, car and truck expenses, commissions and fees, depreciation and section 179 expense deduction(auto), insurance(not health insurance for the owner), interest, legal and professional services, office expenses, rent or lease expenses, repairs and maintenance, supplies, FICA taxes on any employees, medical license(s), travel, meals, and entertainment expenses.

In regards to health insurance for the sole proprietor, it is a deductible expense, but note it is NOT deducted on Schedule C.

A sole proprietor with no employees can deduct 100 percent of the premiums for health insurance for himself, his spouse, and any dependents under the age of 27. The taxpayer can’t be covered by any other health insurance, and the premium can’t exceed the profits of the business. The deduction is taken on Line 29 of Form 1040 or 1040A, and a taxpayer doesn’t have to itemize deductions to qualify

Additionally, some expenses may only be partially deductible, such as the cost of a vehicle, or cell phone used for both personal and business purposes.

I recommend you keep hard copies of your documentation for each expense in a bank box or you can use cloud-based services to scan and store these documents.

It is a good idea to use an online accounting-bookkeeping program like Quickbooks for The Self-Employed for tracking your expenses, at $30/month it is worth it. Wave Accounting offers a free version but I don’t have any experience with it.

The most expensive option will be to hire a bookkeeper and accounting service to manage all of this for you.

Part III – Cost of Goods Sold

If your business sells products, you’ll need to complete Part III of Schedule C. This section is used to calculate the cost of goods sold (COGS), which is the cost of the products you sold during the year. To calculate your COGS, you’ll need to take into account the cost of the raw materials, labor, and other expenses that went into producing the products you sold.

This won’t apply to most of you, endless you are selling supplements, pharmaceuticals, books, or other healthcare-related items.

Part IV – Information on Your Vehicle

If you used a vehicle for business purposes during the year, you’ll need to complete this section of Schedule C. You’ll need to provide information about the vehicle, including the make and model, the date it was placed in service, and the total miles driven during the year.

You’ll also need to provide information about the expenses you incurred for the vehicle, such as the cost of gas, oil changes, and repairs. You’ll have the option to deduct your vehicle expenses using either the standard mileage rate or the actual expenses method.

Part V – Other Expenses

In this section, you can report any other expenses that were not included in Part II or Part III of Schedule C.

Part V provides a range of expense examples that cover a wide array of business-related costs. By familiarizing yourself with these examples, individuals can ensure they are taking full advantage of every eligible deduction available.

Some Specific examples of the “other expenses” for you as an individual physician business include:

-

Bank Fees

-

Cell Phone

-

CME

-

Credit Card Fees

-

Business related Dues and Subscriptions

-

Internet

-

Medical Business Equipment like a Stethoscope or pocket ultrasound, etc…

Line 30 Expenses for Business Use of Your Home

You do have the option of deducting home office use of your home, but in order to do this, you must keep in mind the definition of your home office location. Just because you work at home doesn’t mean you can write off all the power and water bills in your house. The IRS has very precise language regarding what expenses are allowed for a home office tax deduction:

-

First, the area you use for work in your home must be your principal place of business

-

Next, you can only deduct expenses for the portions of your home that are exclusively used for business

-

You can’t work for four hours in your kitchen and deduct your new refrigerator, for instance

-

You must have a dedicated area that you only use for business, and only expenses generated by that area can be used on Form 8829

Summary

The final part of Schedule C is the best part because it is used to summarize your income, expenses, and other deductions. You’ll need to calculate your net profit or loss for the year by subtracting your expenses from your income. If you had a net profit, you’ll need to include this amount on your personal tax return as income.

In the end, this entire process will reduce your taxable income reported on Form 1040 and ultimately you will be paying less taxes than if you received the same income as a W-2 employee.

[/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section]